Before you go and buy the farm

Land is a misunderstood investment. Whether it's a pension fund or sovereign wealth fund, a private equity fund or a sugar company, investors struggle to understand the best way to invest in agriculture. Bain & Company analysis has identiied four approaches that public companies are taking. As we explain in this report, none of the approaches is perfect—each has its own bene?ts and challenges.

Land is fundamentally different from other real asset classes: It is finite. People have been mining precious metals and adding them to the global stocks continuously for millennia. Yet, other than a few well-known reclamation endeavors in the Netherlands and some other highly urbanized areas, we are not creating more land surface.

Unlike other productive assets, land does not depreciate. In fact, it usually appreciates over time, reflecting underlying inflation, demographic demands and gains in agricultural yields from modern farming techniques.1 Some economic historians say that the price of land and the wages paid to unskilled labor are the best references for understanding and updating the value of money over extremely long periods of time (a century or longer) and are much better gauges than the price of gold, Treasuries or even formal inflation indexes.

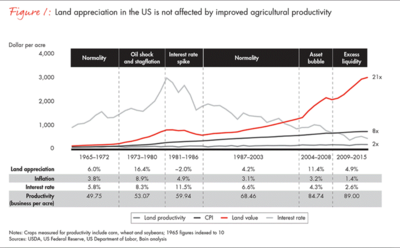

Consider the example of land investments in the US, a country with long statistical records, moderate or low inflation throughout the 20th century, and institutional and financial continuity. Based on Bain & Company analysis, a hypothetical investment in US farmland in 1965 would have yielded a 21-fold return to its holding family or institutional investor until 20152 (see Figure 1). That is an annual CAGR of 6.5%. The main factors influencing the value of the land are interest rates, inflation and land yields.

Those are hardly stellar returns. In addition, they are contingent on a theoretical exit (divesture) at or around market reference values. A poorly timed exit—for instance, at a time of generalized or localized financial distress—can eat away at portions of those returns.

Nevertheless, individuals and families throughout history have acquired, owned and cultivated land, and passed it on as their wealth, inheritance and legacy to future generations. But is there a best way to invest in land?

The rise of corporate farming

Any discussion of land investments should begin with corporate farming. The history of corporations in agricultural development is almost as old as the history of the first European corporations. Some of the world’s first large mercantile corporations, such as the East India Company (British) and the Dutch East India Company, owned not only trading monopolies, fleets and sizable private armies but also had claims to territories and lands that were often developed to either support local company bases or to produce the commodities to be exported back to Europe.

Land investments by corporations significantly increased in rhythm and scope in the late 19th and early 20th centuries. At that time, the invention of steamships, railways and internal combustion engines shrunk relative distances and freight costs around the world. Within a generation, the business of importing fresh and exotic bananas or pineapples to feed a burgeoning middle class in North America and Europe went from a physical impossibility to extremely lucrative. The late 19th century was also a time of premature economic globalization, with abundant European or North American capital deployed rapidly into infrastructure, utilities and agricultural projects in less developed countries and colonies.

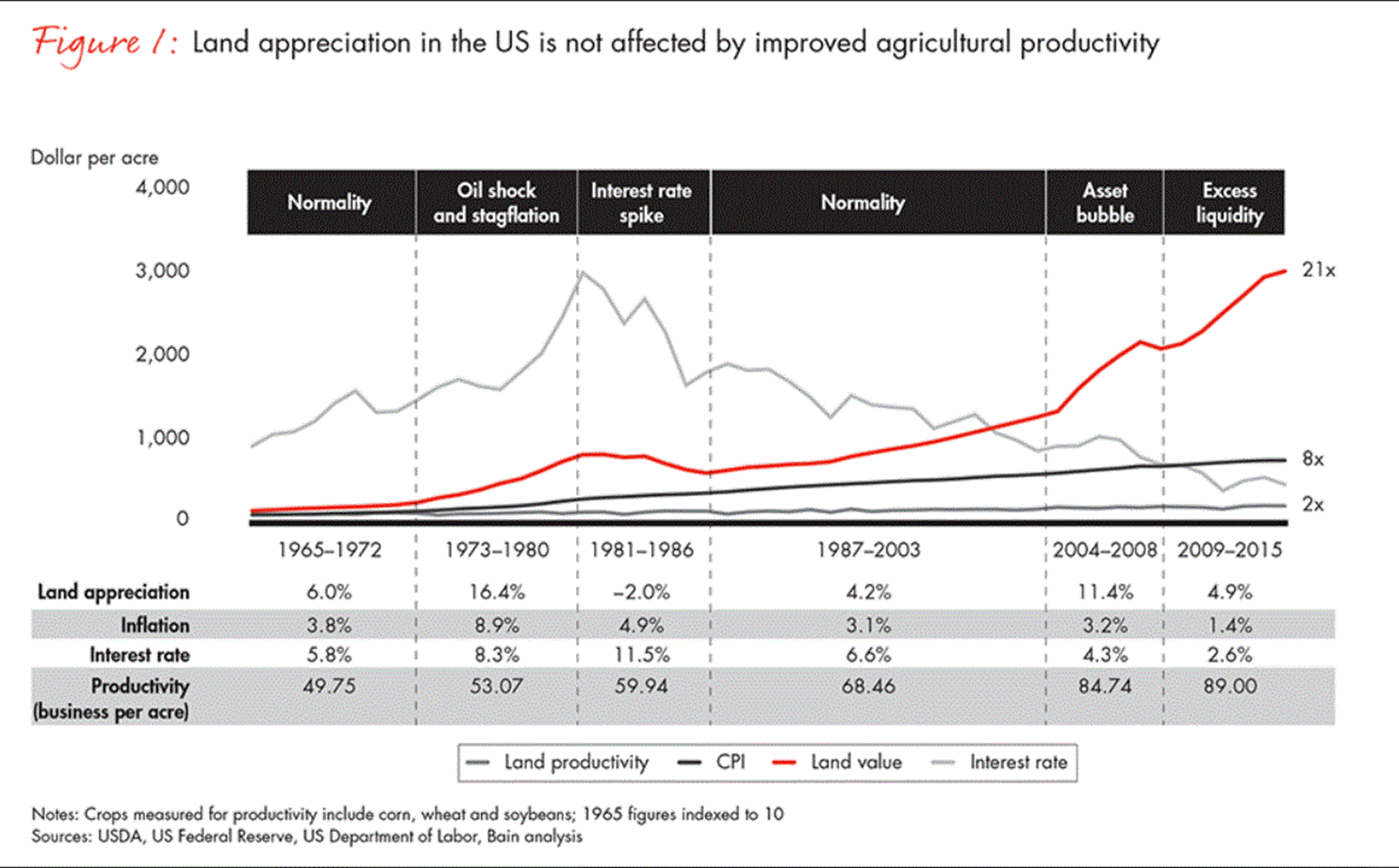

The entity that became the United Fruit Company and more recently Chiquita Brands can trace its inception back to 1871, when an American rail tycoon signed a contract with the government of Costa Rica to build and operate railways. Soon the company was also developing banana plantations—at first to feed railway workers but ultimately to export back to the US. United Fruit was perhaps the most famous and controversial of all big-capital plantation enterprises.

Mostly from around 1870 to 1929 (although some as late as 1940), companies, tycoons and wealthy families were granted, bought or leased vast tracts of land around the (mostly tropical) world, and implemented agricultural-industrial projects in rubber, cocoa, bananas, palm oil, coffee, sugarcane and timber. Some of these companies or their successors still exist today. Others slowly morphed into consumer products or trading companies, shedding their land holdings along the way (see Figure 2).

These were not the only entities acquiring land in those times. In the 19th century, corporations building the tracks for US railroads were granted over 140 million acres of public land. But unlike the bananeras,3 the rail companies never meant to manage farms or plantations. They swiftly sold that land to settlers and used the proceeds (at least in part) to finance construction of the rails themselves.

All of the early cases of corporate ownership of agricultural land reflected one or more of four distinct dimensions, a situation that continues today (see Figure 3).

Land involves high upfront capital requirements and long gestation and payback periods

Agriculture is a capital-intensive activity, both in the form of the working capital required to finance fertilizers, seeds and other inputs through the annual campaign as well as the long-term capital for equipment, machinery, silos and the acquisition and maintenance of the land itself. Tropical cultures, commercial reforestation and temperate climate orchards also need massive capital to build the biological stock. Depending on the culture, each hectare requires investments of $1,500 to $5,000 to clear the land, adjust the soil acidity and plant and nurture the trees until they begin production.

Once they enter their production phase, usually four to seven years after seeding or planting, the plantation will still require annual expenditures similar to the ones incurred by row crop farmers, including fertilization, weed control, soil correction and harvesting (often by manual laborers). That additional capital intensity often yields higher cash margins when the plantations mature.

Strong balance sheets and the ability to raise long-term debt or other forms of financing put corporations in a relatively good position to weather these four to seven years of significant cash outlays.

Industrial processing is needed near the farm

In many of these crops, a first-step conversion process is required, and it needs to happen near agricultural production either due to crop perishability or to minimize the transportation costs for low-valued commodities (or both). Consider sugarcane and the fruits of the oil palm. If not quickly milled, both will perish, and only a small fraction of the harvest will turn into a salable product. Coffee beans must be dried and roasted. Latex must be coagulated and dried. With some of these processes, high industrial asset utilization is critical for profitability. Owners of these assets prefer to also own or lease land to control a share of the agricultural production and ensure a stable supply.

R&D, a potential source of differentiation, may not be commercially available

Commercial cultivation of row crops such as maize, wheat and rice occupy vast land extensions4 and usually receive more than adequate private and public funding for R&D to deliver seeds, traits, fertilization, equipment development and farming techniques. The results of these R&D investments are quickly made available to commercial farmers across the world. But leading-edge R&D results typically are not a source of differentiation for growers.

The situation is different on plantations, where long crop cycles and relatively smaller planted areas indicate that R&D must be fully or partially funded by the corporation and then used for proprietary gains. For example, the largest South American sugar companies invest millions of dollars annually in varietal and equipment development to lower their costs and increase yields. The same is true for eucalyptus pulp growers in Brazil. Increasingly, the results are kept secret or patented and become an important source of differentiation for the owners.

Are publicly traded corporate landowners the right investment vehicle?

The 21st century brought with it a new wave of corporate farming. Like their predecessors from earlier centuries, these corporate farms also bloomed during a period of increased globalization, an uptick in trade flows, decreased transportation costs and, most important, abundant capital.

Unlike their predecessors, however, they were not linked to rail companies, and many of them primarily deal in row crops such as soy, corn, wheat, peanuts and rice. These crops required no immediate processing, and the capital cycles were not significantly longer for corporate owners than they would have been for an average individual or family grower.5

These companies funded themselves with equity from wealthy family funds, sovereign wealth funds and other medium- and long-term investors, as well as shorter- term investors such as private equity funds. The most audacious of these firms became listed on stock exchanges in South America, North America, Russia and Asia. This new wave of farm owners raised major questions for investors:

Are publicly traded corporations the most appropriate vehicle for institutional capital investments in agriculture?

If so, under which circumstances or in which crops?

One argument for the involvement of public corporations in annual row crops is that scale matters more than ever. Indeed, powerful economies of scale are at play in the consolidation of farms: higher utilization levels for equipment, better management of storage capacity, purchasing power for inputs and selling power for outputs. Pictures showing 40 or more machines harvesting and sowing very flat and very vast farms in South America have captured the imaginations of sector observers around the world.

As one agricultural equipment assembler explained, “The economics of new technologies in agriculture disproportionally benefit scale players. My largest seeder in 2002 was able to seed 400 hectares in a month. My typical equipment today does 4,000 hectares. Only very large farming units can truly benefit from such machinery.” Meanwhile, the general manager of a farming company said, “We can pay for a Bloomberg terminal. Our trader speaks English and sits in the city. Two of the largest traders have offices within blocks from us. All of this matters. Last year we helped some of our smaller neighbors sell their production out of a policy of being good neighbors.”

In many situations, small farms are at a distinct disadvantage. For example, a 2014 Bain study in Brazil determined that the largest corporate farmers in the Mato Grosso region were able to sell their production for $15–$20 per metric ton above the prices obtained by small farmers.

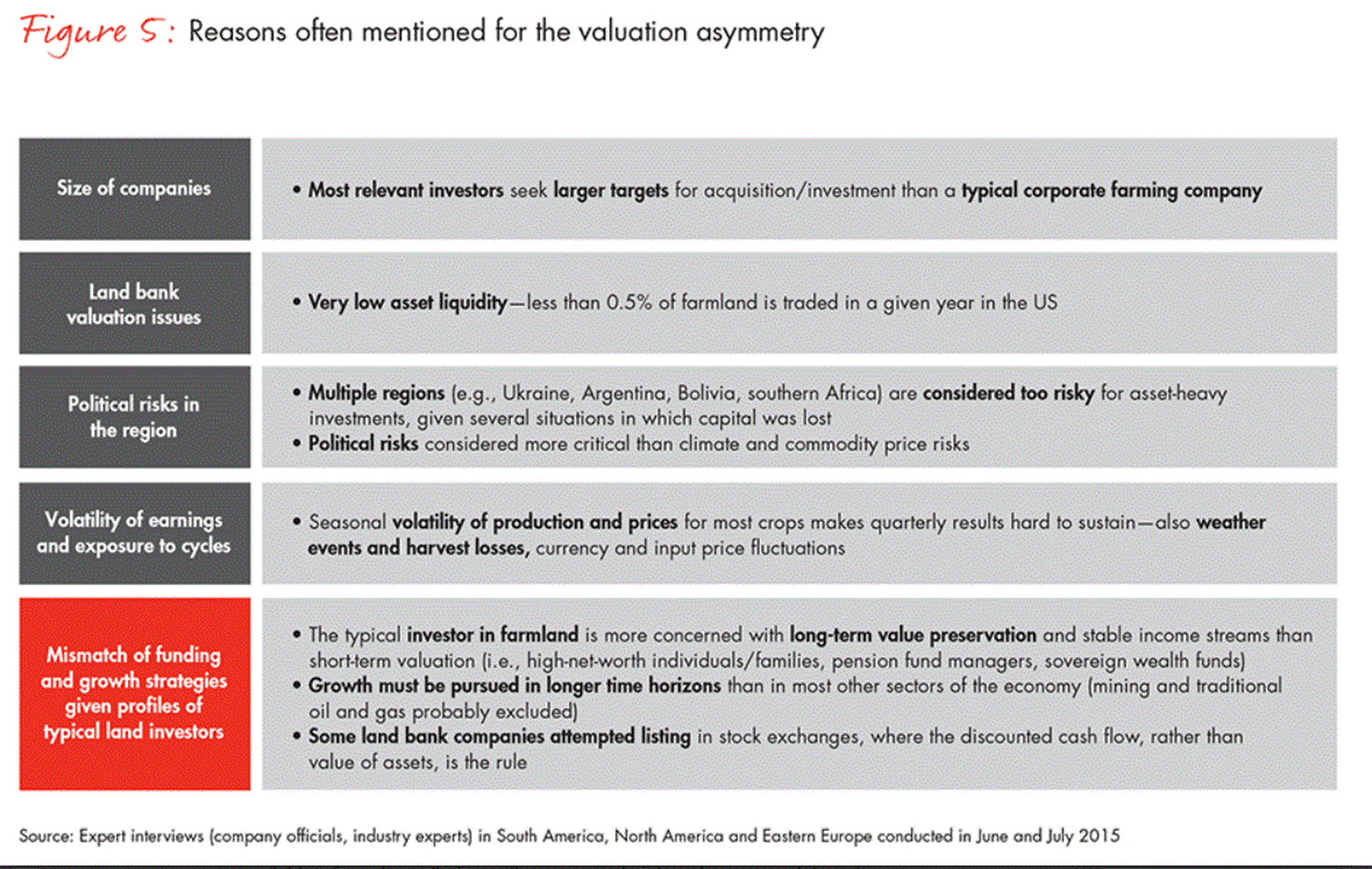

For all their scale efficiencies and other advantages over local farmers, however, most new farm corporations have failed to achieve fair valuations. We analyzed the performance of 11 land and agricultural companies and determined that only two of them traded at or above their accounting book value. The few companies in our sample that traded at a premium either have significant industrial assets beyond farming or are active in long-term cash commodities such as citrus (see Figure 4).

Our findings suggest that these companies and investors would be better off if they cautiously divested their farms at market reference values. The findings also indicate that some investors (most of them farmers) are willing to pay more for land and accept a lower yield on their investment than the typical equity investor would.

Understanding the reasons behind this systematic discount not only solves these companies’ valuation issues but also sheds light on the possible path to liquidity for many privately held farming companies. With those goals in mind, we interviewed sector executives and equity analysts as well as active and passive investors in agricultural land for their insights (see Figure 5).

We believe that most of the reasons mentioned by our interviewees would apply to any given company we surveyed. The last item on the list—the mismatch of funding and growth strategies—appears to be particularly relevant given how institutional fund managers are usually organized. For example, among the largest fund managers, investment officers knowledgeable about agriculture and responsible for land investment decisions may not be the same individuals or group who are deciding on equity markets allocations.

How are the affected companies coping with the valuation discounts? Based on publicly available information—that is, with no access to internal company data or to management—we mapped the strategic moves of four agricultural companies, each of which represents a different approach:

- SLC Agrícola operates a leasing model.

- Adecoagro applies value chain diversification (as does Amaggi).

- BrasilAgro employs land conversion.

- And Radar (a subsidiary of Cosan) utilizes real estate investment trusts (REITs), timber investment management organizations (TIMOs) and institutional investors.

We selected these four companies because together they demonstrate four distinct and potentially viable ways in which farming companies are trying to outgrow their valuation challenges.

Leasing model

This strategy expands production on leased or rented land to grow top and bottom lines without expanding the asset base and thus generates higher asset turns and returns to shareholders. A growing number of agricultural estate owners in the Americas lease out their lands to professional operators—or to more entrepreneurial neighbors. This is a long-established practice in Argentina, where a family may live in Buenos Aires and lease its land to very large farming operators. More recently, many of the most competitive sugar mills in Brazil no longer own the land where they grow their sugar. And it is happening in the US and Canada, where the most professional and successful farmers either buy or lease their neighbors’ properties.

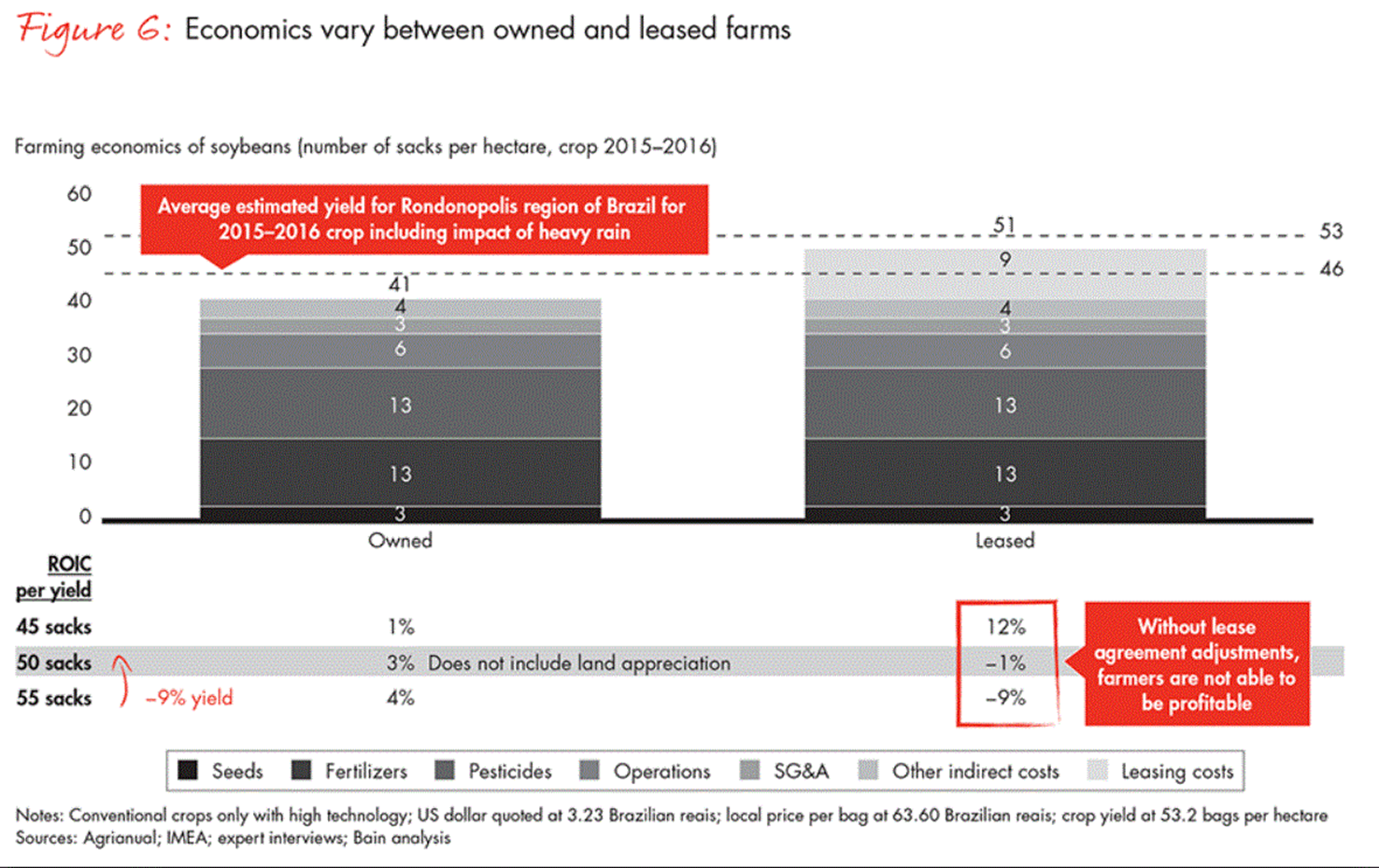

But this needs to be done with utmost care. The typical operational leverage implied in the leasing terms can easily cripple a lessee in the event of a harvest loss, especially for crops and locations with low profit margins. We’ve analyzed the economics of a hypothetical farmer in Mato Grosso, Brazil, in both leased and owned situations (see Figure 6). While the return on invested capital of a leased farm can be attractive, a local yield loss of only 9%, if not compensated by increased commodity prices or leasing renegotiation, is enough to compromise (potentially fatally) the farmer’s cash returns. That is because the value chain margins in Mato Grosso are much lower than the margins of more profitable regions such as the Santa Fé region of Argentina or the US heartland.

Furthermore, managing farms seems to be a local business, with local competency requirements that will vary by state or province or even by county or municipality. Many operators who have tried to ramp up leasing models across a nation or continent have failed. The high operational leverage implied in leasing, combined with the difficulty to ensure consistency of operations and yield across regions, can be daunting. Companies scaling nationally have met a higher degree of success when they buy rather than lease the farms they operate.

Value chain diversification

Some large farmers and farming companies, especially in South America, have expanded along the value chain into grain origination, corn and soy processing, and even export logistics. Amaggi, perhaps one of the most prominent, is not only a mega farmer with 233,000 hectares of mostly owned land under cultivation but also an important oilseed originator and logistics operator in the central-west region of Brazil that has participated in joint ventures with some of the world’s leading export oilseed traders.

If well timed and executed, some of these moves can be very rewarding. But expanding along the value chain takes a company beyond its core business, which means facing different competitors and customers and managing a cost base and a balance sheet that will be very different from farming. The competencies required to manage those businesses will be distinct. Empirical evidence across industries shows that diversification moves often fail.

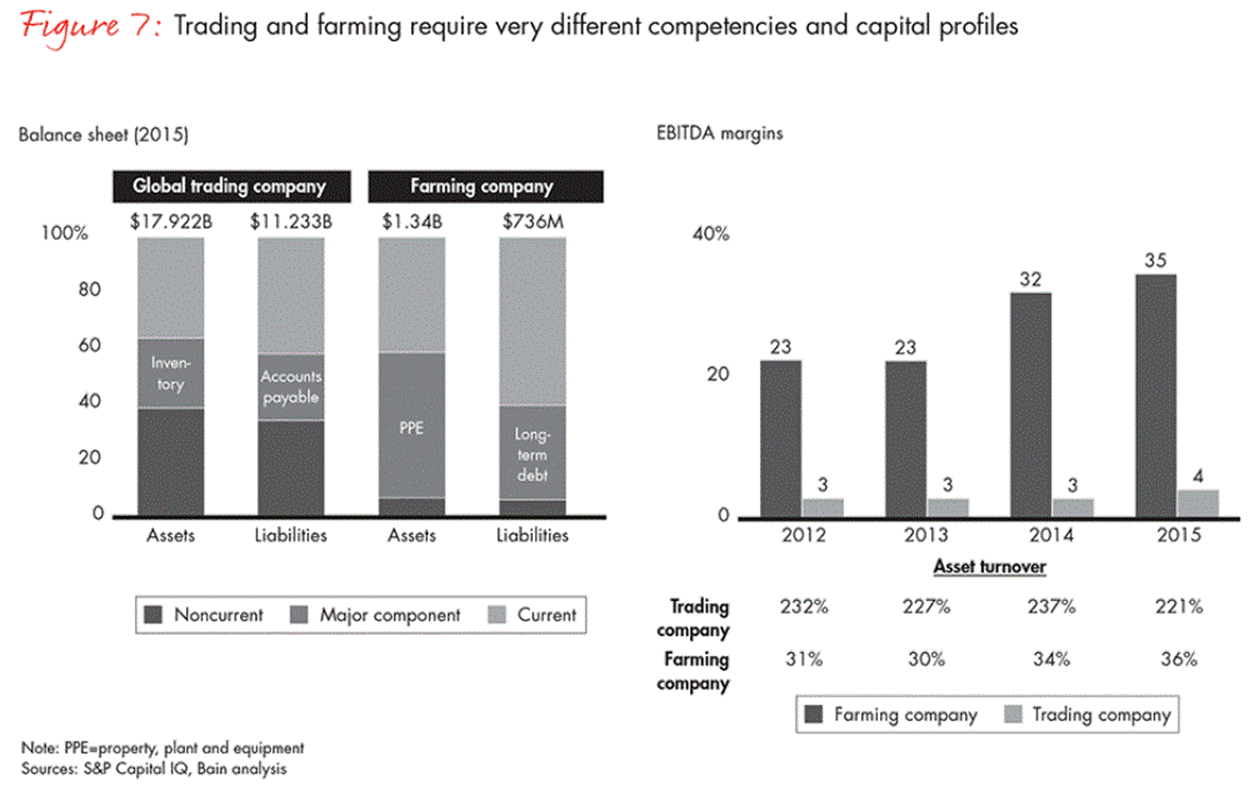

We compared the balance sheet of a prominent farming company with that of one of the world’s leading grain trading houses (see Figure 7). The composition of the balance sheet and key margin and asset turnover indexes highlights the distinctions between the businesses of farming and trading.

Land conversion

This is the agricultural equivalent of urban real estate development. It begins with the acquisition of relatively cheap land, usually degraded pastures or lightly forested land. The investor will then clear the land, correct soil acidity and farm the land until it can be rightfully considered high-performing row cropland. The land is then sold to another class of investors. A full cycle will run for five years or more.

Land conversion may not be a concept in North America, where most agricultural regions were developed decades ago, but it has been common in South America over the past decade, given the accelerated ramp-up of agricultural production in Argentina, Brazil, Paraguay, Bolivia and Colombia.

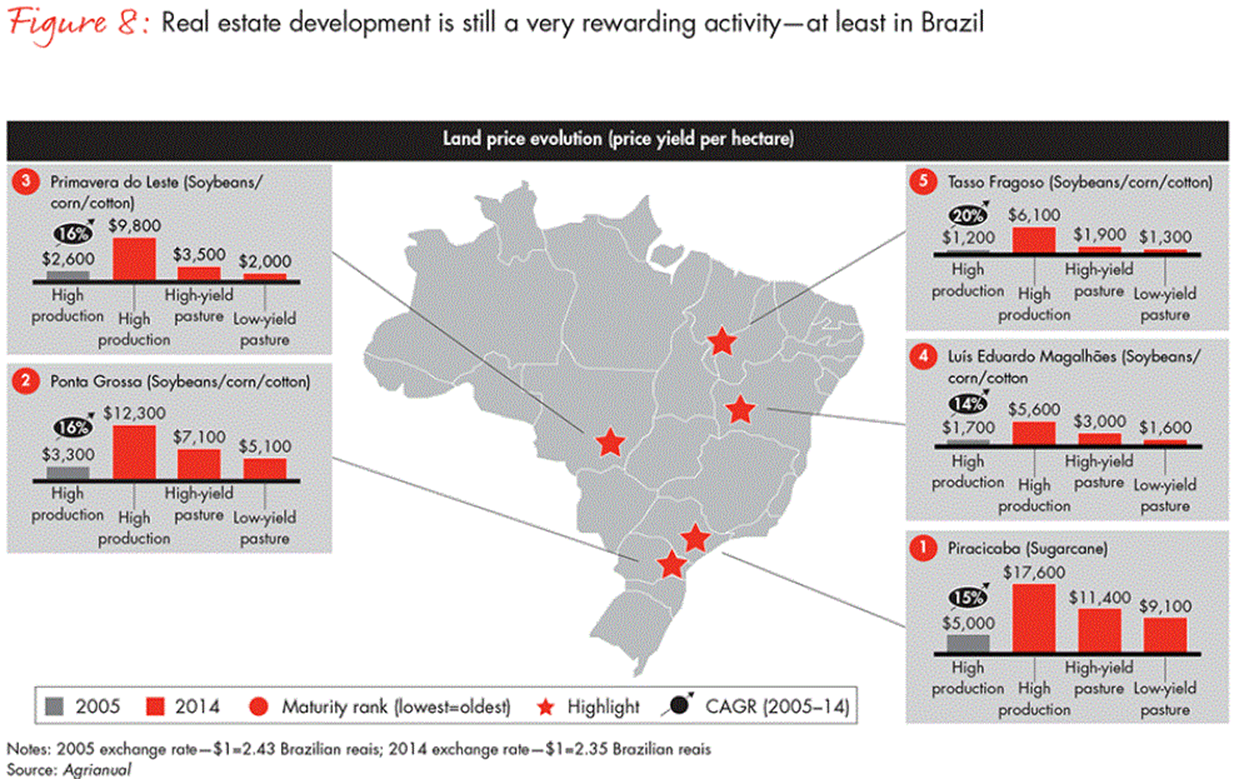

Brazil is the most developed agricultural market in South America and also the only country in the region with reliable land price and yield statistics. Companies and players active in land conversion in Brazil have accrued or realized significant economic value over the past 10 years.

Indeed, land prices have increased in Brazil (see Figure 8). In five of the Brazilian agricultural regions we studied, land price trends were consistent within each region— prices rose in all of them, and fertile cropland was more valuable than pastures.

From 2005 to 2014,6 land conversion in South America was a rewarding activity. We calculated the hypothetical cash-on-cash return of land conversion in various Brazilian regions in a range of 3 to 5.5 times the invested capital, in nominal local currency. Some of the farming companies surveyed describe themselves as real estate developers, and they can create significant shareholder value. However, this approach may present challenges. Interviewed executives believe the number of good land conversion opportunities is finite (and not very large to begin with). Agricultural expansion also depends on rising commodity prices that would justify the continual addition of cost-marginal land into the global supply. The long-term prospects for agriculture remain bullish, given the rising global population and increasing incomes, but the growth pace going forward will be slower and probably more volatile than in recent history. This will bring additional challenges to investors in land conversion.

REITs, TIMOs and institutional investors

Another class of investors pouring resources into agricultural and forestry lands are institutional investors such as pension fund managers, sovereign wealth funds and high-net-worth individuals and families. Due to the size of their balance sheets, these investors can afford to hire professional financial advisers. These advisers run asset allocation exercises and determine whether a typically small share of the investable pie should go into farmland or commercial forestry land.

In our interviews with these investors, we learned that they are employing entirely different vehicles to invest in land. For example, they avoid buying equity in listed agricultural companies. Instead, they typically set up or invest in funds with REIT or TIMO features, allowing them to optimize taxes and concentrate on dividend income, which is important to meet obligations to pensioners. They are relatively unconcerned about having immediate liquidity in their investments.

Because land investment bears many parallels with urban real estate, precious metals and art investments, it is not surprising that the bulk of the financial securities that involve land and forestry are in the form of either direct investments by financial investors or in funds such as REITs and TIMOs and not in equity investments. With REITs and TIMOs, valuation vs. accounting book value is not an issue. They do, however, raise the challenge of liquidity and the fact that returns are dependent on a timely and fortuitous exit.

Is land a financial investment with no opportunity for differentiated returns? That is a reasonable conclusion, given the fact that land prices are so closely tied to a few macro-economic variables—interest rates, foremost—and that these variables seem to have reached a bottom.

But we do believe that plenty of localized appreciation opportunities exist for investors who are savvy (or lucky) enough to anticipate trends or triggers. For example, the development of a new logistics corridor that improves the cost position of a given region, the development and spread of a new genetic trait or hybrid seed to a particular region, a shift in consumer preferences that leads to the repurposing of a given region to higher-valued crops—all of which have been documented before in parts of the US, South America and Australia. And they could happen again, but capturing them requires superior and proprietary insight.

Nevertheless, individuals and families throughout history (including one of the authors of this report) have acquired, owned and cultivated land, and passed it on as their wealth, inheritance and legacy to future generations.

--

1 Land may not formally depreciate as an investment in an industrial asset would, but agricultural land can certainly be exhausted, especially if poor agricultural practices are employed. It may then lose value if inherent fertility falls. There are well-documented cases of that in cotton areas of the US and in sugarcane areas in India. There is speculation that farmers in recent decades were consciously exhausting some row crop areas in Argentina.

2 Land prices have an r-square multivariable correlation of 0.82 to inflation, interest rate and land yield.

3 Bananeras is the Central American term for US companies that produced and exported tropical fruit.

4 As of 2015–2016, rice occupied 161 million hectares globally vs. 26 million hectares dedicated for sugarcane.

5 We should recognize that most of these companies were active in South America and that they grew by acquiring raw land and preparing it for farming. That process is also capital intensive, but that capital will usually be recouped at the divesture of the property.

6 We run this analysis up to 2014 instead of 2015 because the currency and economic volatility in Brazil that began in late 2014 are impacting real asset prices in unpredictable ways and must still run their course.

Fernando Martins and Scott Duncan are Bain & Company partners based in Chicago and leaders of the Agribusiness practice in the Americas.

The authors extend gratitude to all who contributed to this report—in particular, Adriane van Houten, a Bain consultant based in São Paulo; Sunadda Vanaphongsai, an associate consultant in Bangkok; and João Panisi, a senior associate consultant in São Paulo.